Corporate Mortality and the Culture of Failure

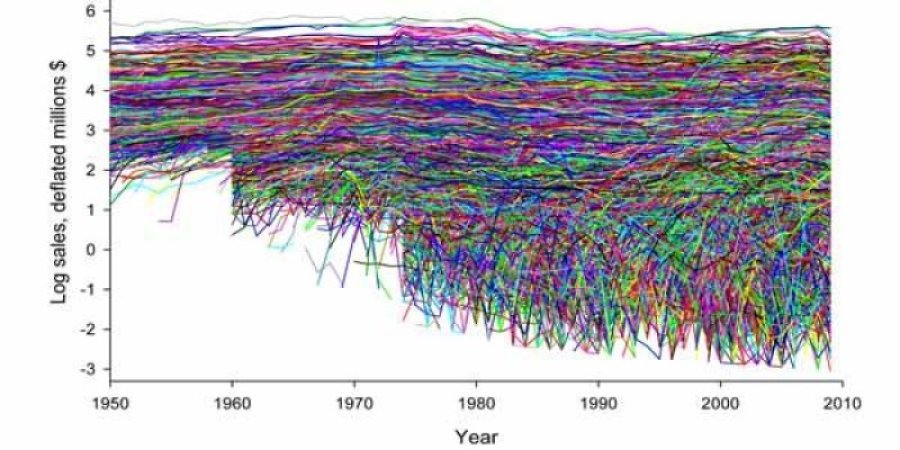

Sizes of some 30,000 companies traded publicly on US markets from 1950-2009, measured by their sales (controlling for inflation and GDP growth). The relatively rapid growth of smaller companies near the beginnings of their lifespans account for the ragged lower portion of the chart, as well as the relatively steep initial sales increases. As companies reach maturity, their sales tend to level off.

Credit: Marcus Hamilton and Madeleine Daepp

What about failure?

When I was writing my article on entrepreneurship in Egypt (Peterson 2010), which I heavily cannibalized for Chapter Six of Connected in Cairo, one of the things in which I was particularly interested in was failure.

One of my key points was that when US companies fail at home, that’s just business. But when they fail while doing business in Egypt or comment on the failures of Egyptian entrepreneurs–and I suspect this holds in many countries–they blame it on the local “culture.” Egyptian business failure is blamed on a supposed poor work ethic, on institutions like wasta, and on a presumed “lack of entrepreneurial imagination.”

When I sought to contextualize the discourse of these businessmen with some general statistical data, I was shocked to find almost nothing on business failures.

Obviously all businesses dies sometime, and every entrepreneurial adventure is by definition a risk, yet there was not only no theoretical literature on entreprenuerial failure, there were no statistics. And none on business failures generally.

Well now there is (thanks in part to another anthropologist). It turns out the average publicly traded company in the US lasts only ten years.

The Life Span of Companies

Eve n more interesting, the interdisciplinary team of two physicists, an anthropologist and an economist at the Santa Fe Institute in New Mexico discovered that companies die off at roughly the same rate regardless of size, what kinds of products or services they produce, how long they have been in business, or how well-established they are.

n more interesting, the interdisciplinary team of two physicists, an anthropologist and an economist at the Santa Fe Institute in New Mexico discovered that companies die off at roughly the same rate regardless of size, what kinds of products or services they produce, how long they have been in business, or how well-established they are.

This finding runs counter to the few theories that exist in business literature, which either assume that newer, less established companies are more vulnerable, or that more established, less flexible companies are more vulnerable.

Causes of death include:

- being bought up (the most common),

- merging with another company

- filing for bankruptcy

The researchers analyzed figures from Standard and Poor’s Compustat, a database containing 65 years of information about publicly traded companies on the New York Stock Exchange.

Of course, the majority of corporations–including those I studied–are privately held. And since there is no comprehensive source of data for such companies–they don’t have to report to shareholders, after all–it is impossible to tell if entrepreneurship yields similar results (my own guess is that privately held companies die off at a faster rate, but I can’t prove it).

One thing this study does, however, is provide support for my insistence that American businessmen who ascribe business failure in Egypt to local “culture” have no leg to stand on.

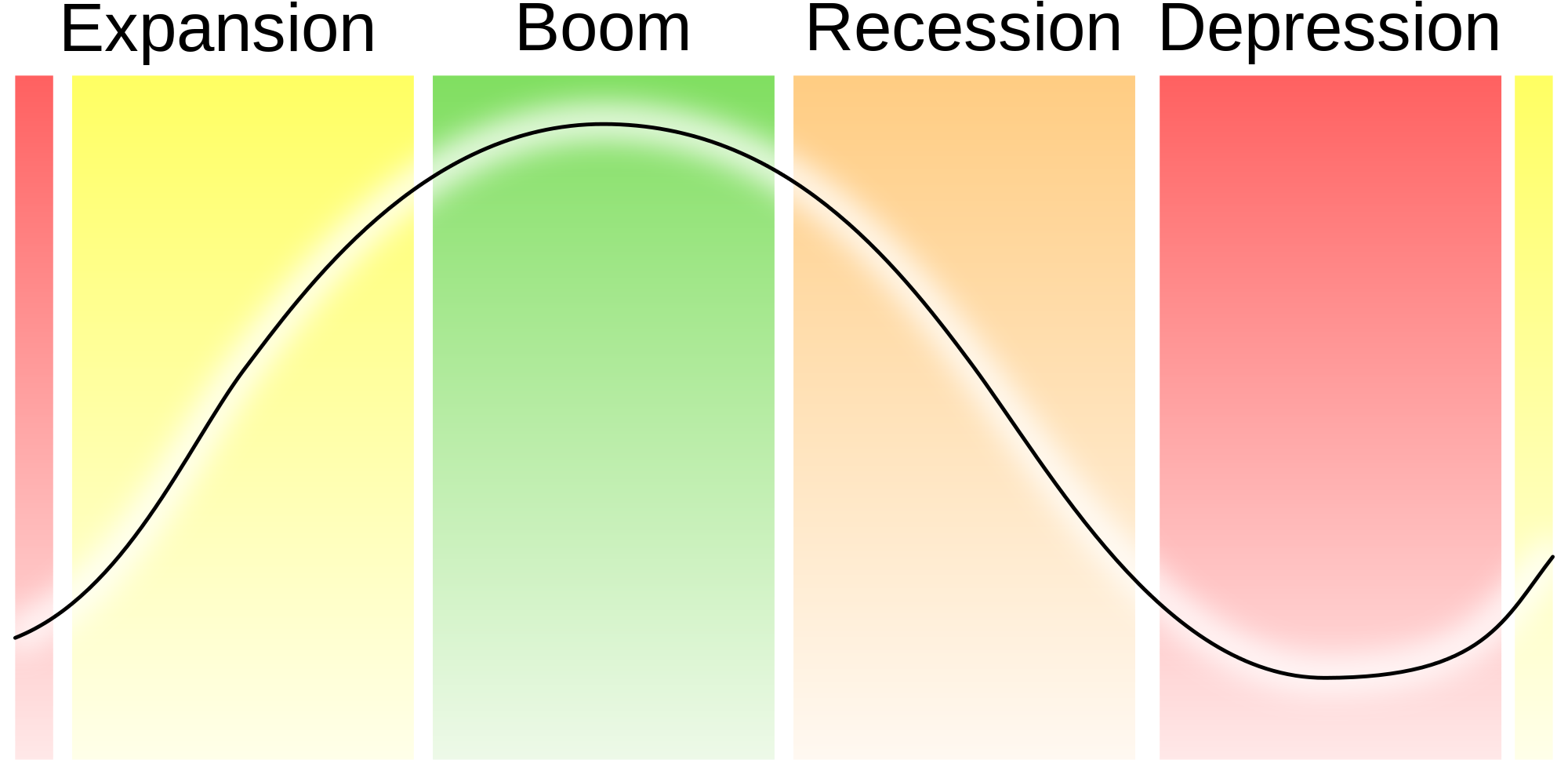

The Business Cycle

This boom and bust cycle is a well understood phenomenon under capitalism worldwide. One or two entrepreneurs have an idea, raise capital and create successful businesses. Once their successful model is established, other entrepreneurs imitate it, with variations, saturating the market and ultimately making the venture significantly less profitable.

This boom and bust cycle is a well understood phenomenon under capitalism worldwide. One or two entrepreneurs have an idea, raise capital and create successful businesses. Once their successful model is established, other entrepreneurs imitate it, with variations, saturating the market and ultimately making the venture significantly less profitable.

One can find endless examples of this in Egypt from the overexpansion of Red Sea resorts to web development companies (Peterson and Panovic, 2004) to fad food stores like pizza and sushi. As the economist George Barclay Richardson put it:

“a general profit opportunity, which is both known to everyone and capable of being exploited by everyone, is, in an important sense, an opportunity for no one in particular” (1960: 57)

Bad for businessmen perhaps, say many economists, but good for consumers because increasing competition reduces prices.

The American and British businessmen critiquing Egyptian entrepreneurs may be correct in thinking that there are structural issues in Egypt that make business failure more likely. but if so they are linked to the economic environment rather than to cultural values and learned behaviors. Egypt has an extremely modest consumer base, in which only 5% of Egypt’s population can afford transnational consumer goods (Osman, 1998), and the top 3% of Egypt’s population accounts for half its consumer spending (Bartsch, 1997). This may make the boom-and-bust cycle far more precarious than in the Western countries from which this model is drawn.

Not so my international interlocutors in Egypt. They imagined the chaos as structured into “business cycles” and understood entrepreneurs as important, even heroic figures in these cycles.

It’s All Schumpeter’s Fault

According to the business cycle model, business people engaged in two types of behavior: routine following of business norms and practices, and innovation through disruption of these routines. The business cycle emerges from a tension between businessmen as creative entrepreneurs and rational economic being,s because entrepreneurs imagine innovation but they will only proceed to put these innovations into practice if they perceive that relevant economic conditions are stable enough to ensure profitability.

According to the business cycle model, business people engaged in two types of behavior: routine following of business norms and practices, and innovation through disruption of these routines. The business cycle emerges from a tension between businessmen as creative entrepreneurs and rational economic being,s because entrepreneurs imagine innovation but they will only proceed to put these innovations into practice if they perceive that relevant economic conditions are stable enough to ensure profitability.

Yet innovation disrupts routine in many ways, since one entrepreneur’s vision, successfully employed and producing a period of profitability, will necessarily be imitated, reducing overall profitability not only for the initiator but for all the imitators. This cycle also occurs on a large scale: when there is a great deal of innovation and imitation, uncertainty about profitability increases. This reduces the likelihood of entrepreneurs acting on their visions, and plunges the economy into recession and depression. Even as these downturns stabilize the economy by increasing coordination between economic activities, ideas for innovation accumulate, leading to another period of growth and prosperity.

This views are largely informed–whether or not they’ve ever heard of him–by the Austrian school theorist Joseph Schumpeter, whose work still is the main resource in the economics of entrepreneurship.

For Schumpeter, as for those who critiqued and extended his theories after him (e.g. Kirzner 1973), entrepreneurs drive the economy by being just a little more perceptive and daring than most other business people. Schumpeter saw entrepreneurs as the sources of technological change and prosperity in capitalist society, calling them “wild-spirits” and “fiery souls” in homage to their creativity, and assigned them an almost heroic role in the business cycle.

He preferred the German unternehmer (“one who undertakes”) to the French “entrepreneur,” and coined the term unternehmergeist (“entrepreneurial spirit”) to describe the capacity of such individuals to innovate and produce change.

Weirdly–and out of sync with reality–Schumpeter assumed that the entrepreneurial imagination “though inexplicable, was always correct” (Loasby 1996: 17).

If only. My own experiences growing up in the US, and studying business and change in Egypt and India, makes me all too aware of how the entrepreneurial imagination can be wrong.

Of course, I don’t really believe in business cycles. I think some kind of ecological model of businesses engaged in competition within an environment which includes, but is not limited to market activity, would generate more interesting and authentic perspectives.

Hopefully, statistical studies of business mortality will help bring some much needed correctives to the study of entrepreneurialism and business cycles that will put these theories on sounder empirical and analytical ground.

References

Bartsch, U. 1997. Interpreting household budget surveys: Estimates for poverty and income distribution in Egypt. Working Papers of the Economic Research Forum for the Arab Countries, Iran and Turkey, No. 199714, Cairo: ERF.

Daepp, Madeleine I. G., Marcus J. Hamilton , Geoffrey B. West , Luís M. A. Bettencourt. 2015. The mortality of companies. Royal Society Interface

Kirzner, Israel M. 1973. Competition and entrepreneurship. Chicago: University of Chicago Press.

Loasby, B.J. 1996. The imagined, deemed possible. In E. Helmstädter and M. Perlman, eds. Behavioral norms, technological progress, and economic dynamics. Pp. 17-32. Ann Arbor: University of Michigan Press.

Osman, O.M. 1998. Development and poverty reduction strategies in Egypt. Working Papers of the Economic Research Forum for the Arab Countries, Iran and Turkey, No. 199813. Cairo: ERF.

Peterson, Mark Allen. 2010. “Agents of Hybridity: Class, Culture Brokers, and the Entrepreneurial Imagination in Cosmopolitan Cairo.” Research in Economic Anthropology 30: 225-256.

Richardson, George Barclay. 1960. Information and investment. Oxford: Oxford University Press.

Trackbacks